Introduction: Owning a Piece of a Skyscraper

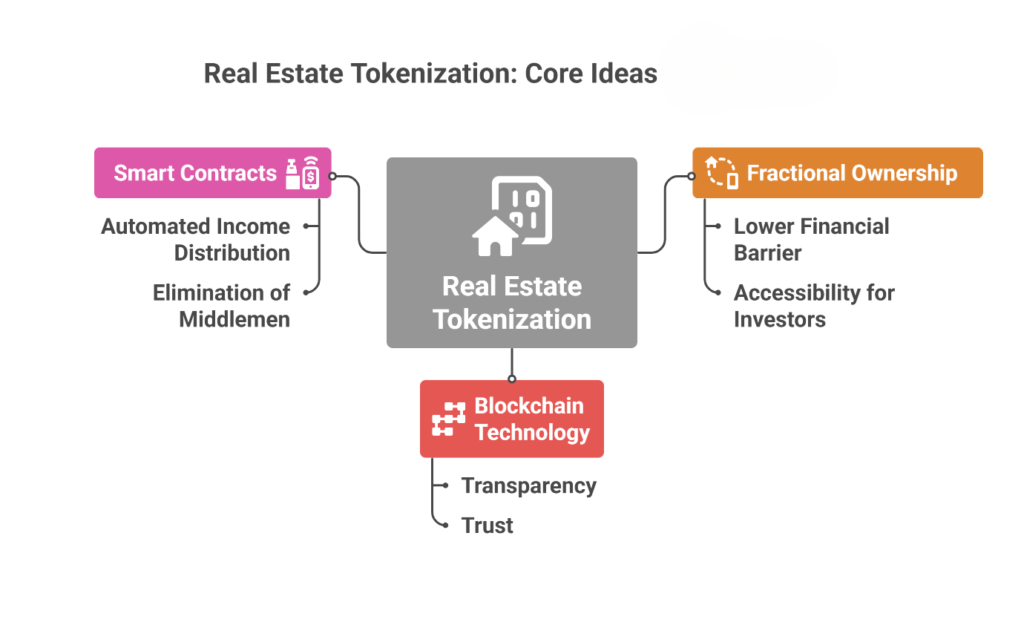

What is RWA Tokenization? From a Whole Building to Digital Bricks

- Fractionalization: This is the key that unlocks access. It is the process of dividing ownership of a high-value asset into smaller, tradable digital units. Instead of needing ₹2 crores for an apartment, an investor could buy a fraction of it for ₹20,000.

- Programmability: Each token is a piece of smart contract code. This allows for automated logic to be built directly into the asset. Rules for dividend distribution, compliance checks, and trading restrictions can be executed automatically without intermediaries.

- Immutability: Once a transaction is recorded on a blockchain, it is unchangeable. This creates a tamper-proof, permanent record of ownership, ensuring data integrity and building trust between participants who don’t know each other.

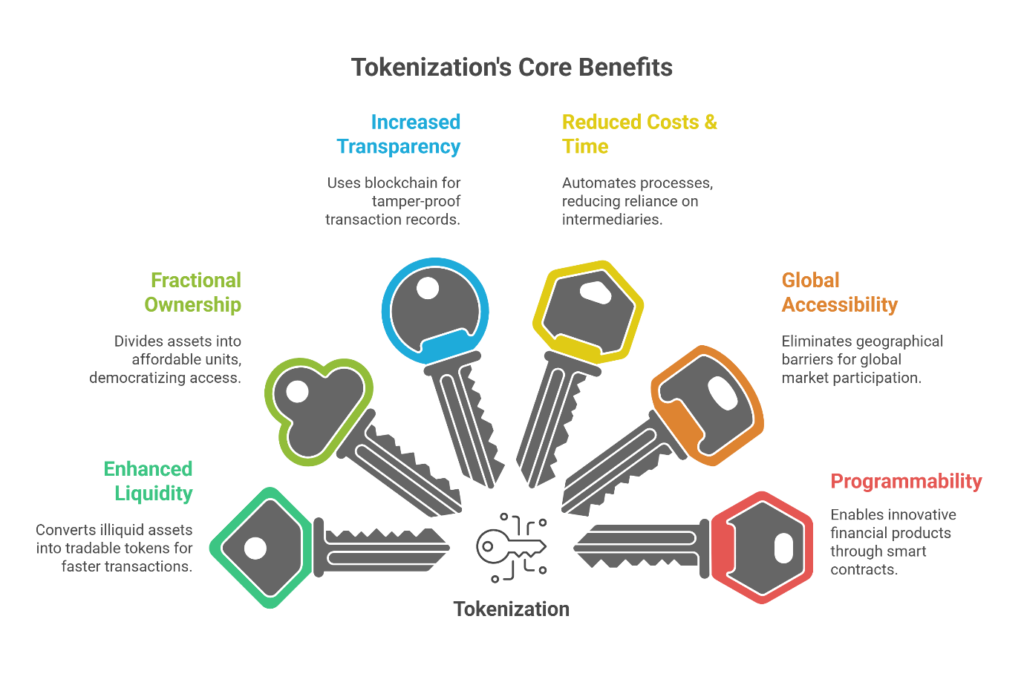

Why This Isn't Just Hype: The Four Pillars of Tokenized Real Estate

The Global Wave: A Multi-Trillion Dollar Opportunity

The momentum behind RWA tokenization is no longer speculative; it is a measurable global trend driven by institutional capital. Projections show this momentum accelerating dramatically.

Tokenization is set to transform the world’s largest asset class—real estate—by converting physical property rights into digital tokens on a blockchain. This process is unlocking unprecedented liquidity and accessibility in a historically illiquid market.

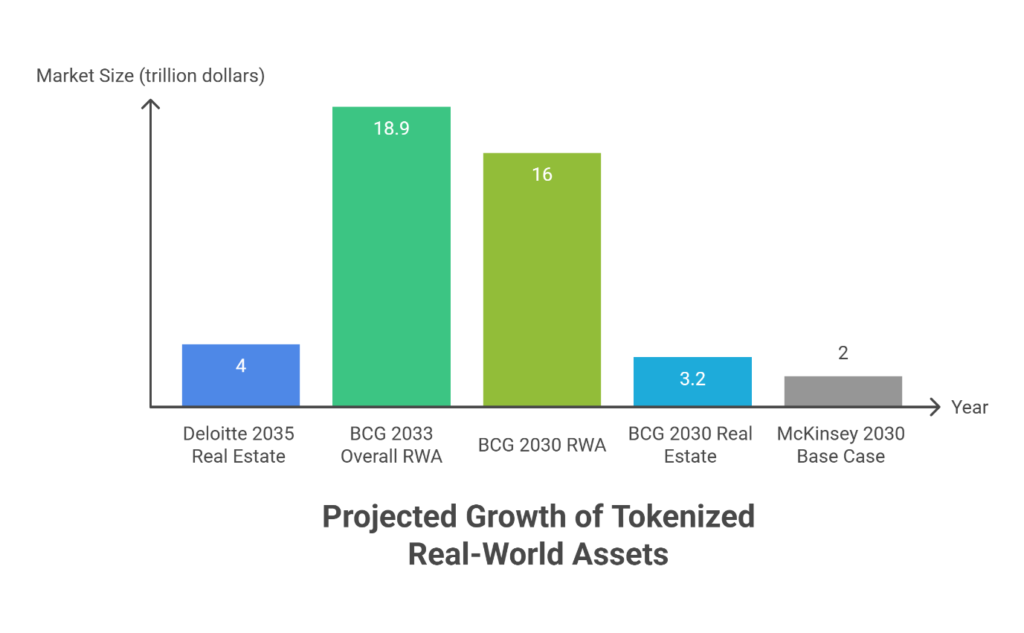

Forward-looking projections confirm that this is just the beginning. The world’s largest financial institutions see tokenization as a foundational shift in how markets will operate.

Leading analytics platforms like RWA.xyz provide clear directional snapshots of market value, showing a value of $25.12 billion as of July 2025 and $33.84 billion as of October 2025.

Currently, this growth is dominated by institutional-grade, yield-bearing assets. Private credit alone accounts for $14.7 billion , followed by treasuries at $6.2 billion. This demonstrates that the core infrastructure is being built to a professional, compliance-driven standard first—a necessary step before broader retail products can be rolled out.

While current figures are impressive, future projections from leading financial analysis firms are exceptionally optimistic, anticipating a multi-trillion-dollar market by the end of the decade.

From Locked Titles to Liquid Tokens: Solving India’s Real Estate Pain Points

- Problem: Extreme Illiquidity and High Entry Barriers.

- Solution: Fractionalization divides a property’s ownership into smaller, affordable digital tokens. This dramatically lowers minimum investment thresholds, allowing individuals to buy into high-value properties with smaller amounts of capital and making it far easier to sell those stakes in a secondary market.

- Problem: Opaque Title Records and Registry Delays.

- Solution: A blockchain provides a transparent, immutable ledger that serves as a national, incorruptible digital registry layer. This “single source of truth” for property titles leapfrogs the need for physical verification and dependence on outdated, non-digitized taluk office records, reducing ambiguity and the potential for fraud. Smart legal contracts can automate the verification and transfer process, minimizing the manual paperwork and bureaucratic delays that plague Indian property registries.

- Problem: Lack of Standardization and Valuation Uncertainty.

- Solution: With readily available on-chain data from transactions, price discovery becomes far more efficient and transparent. An auditable, time-stamped history of appraisals and sales recorded on the blockchain enhances confidence in a property’s valuation, moving it away from subjective estimates toward data-driven analysis.

- Problem: Exclusion of Retail Investors.

- Solution: By lowering investment minimums through fractionalization, tokenization opens up investment in prime commercial and residential real estate to a much broader audience. Young professionals, salaried employees, and even Non-Resident Indians (NRIs) can participate directly in the Indian real estate market without needing to purchase an entire physical asset.

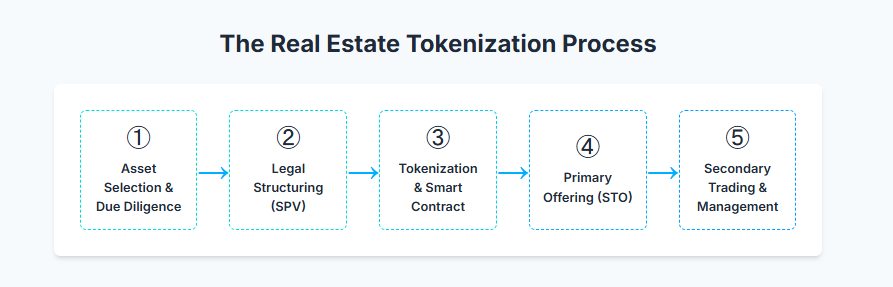

How It Actually Works: A Simplified Use Case

- Asset Selection and Due Diligence: A specific property—for instance, a commercial office floor in Gurugram—is selected. It then undergoes rigorous due diligence. Lawyers verify the legal title for clarity and absence of encumbrances, while certified appraisers conduct a thorough valuation and physical inspection.

- Legal Structuring (The SPV Model): The property’s legal ownership is transferred into a separate legal entity, known as a Special Purpose Vehicle (SPV). This isolates the asset and its ownership from other risks. A regulated custodian then takes legal charge of the physical asset, ensuring the digital tokens are legally and physically backed by a real-world property.

- Token Issuance: Digital tokens representing fractional ownership in the SPV (and thus, the property) are created, or “minted,” on a blockchain. Blockchains like Polygon, which are gaining traction for RWA projects, can be used for this step. Each token is encoded with the rights and rules associated with ownership.

- Primary Offering and Distribution: The tokens are offered to investors in a primary sale, commonly known as a Security Token Offering (STO). Because these tokens are typically classified as securities, this process must adhere to strict regulations. Mandatory Know Your Customer (KYC) and Anti-Money Laundering (AML) procedures are conducted to verify investor identities and ensure compliance with financial crime prevention laws.

- Ongoing Management and Secondary Trading:Following the STO, the smart contract automates key operational tasks, such as distributing rental income or other profits directly to token holders’ digital wallets. The tokens can then be traded on regulated secondary markets or digital exchanges, providing investors with a mechanism for liquidity and price discovery.

Traditional vs. Tokenized: A Direct Comparison

| Aspect | Traditional Real Estate | Tokenized Real Estate |

|---|---|---|

| Minimum Investment | ₹20 lakhs – ₹2 crores | ₹1,000 – ₹10,000 |

| Down Payment Required | 20–30% (₹4–60 lakhs) | 100% (but far smaller amount) |

| Time to Complete Purchase | 3–6 months | 3–15 minutes |

| Paperwork | Extensive (50+ documents) | Digital (KYC + wallet) |

| Liquidity | 6–12 months to sell | Minutes to hours |

| Transaction Costs | 7–10% (stamp duty, brokerage, legal) | 1–2% (platform fees) |

| Access to Prime Assets | Only ultra-wealthy | Anyone with internet |

| Geographic Limitation | Must be local or hire agents | Global access |

| Ownership Verification | Difficult, manual | Instant, on-chain |

| Rental Income Distribution | Manual, subject to delays | Automatic, programmable |

| Property Management | Manual, expensive | Automated via smart contracts |

| Transparency | Opaque, prone to fraud | Fully transparent, auditable |

| Diversification | Difficult (capital intensive) | Easy (buy multiple properties) |

| Resale Complexity | High (valuation, buyers, paperwork) | Low (list and sell like stocks) |

| Settlement Time | Weeks to months | Instant |

| Inheritance / Transfer | Complex legal process | Simple on-chain transfer |

Beyond Finance: The Hidden Benefits

While the financial case for tokenization is compelling, the second-order effects could be equally transformative.

The Environmental and Urban Planning Dimension

Fractional ownership could have surprising benefits for sustainable urban development.

When thousands of small investors own pieces of a building, they have a collective interest in its maintenance, energy efficiency, and long-term value. Smart contracts could even allocate a portion of rental yields automatically toward building maintenance and green upgrades, creating a self-sustaining model for urban asset management.

Imagine a scenario where a building’s token holders vote on installing solar panels. The cost is automatically deducted from rental yields over 24 months. The energy savings increase net income, raising token values. Everyone wins, and the city becomes greener—all coordinated by code rather than committee meetings.

The “Skin in the Game” Social Benefit

There’s an underexplored social dimension here. When young professionals can own even a small stake in their neighborhood—a share of the building they live in, or the commercial strip they shop at—it creates a different relationship with urban space.

They’re not just tenants anymore; they’re stakeholders. They vote on building improvements. They benefit directly from neighborhood appreciation. They have an incentive to maintain public spaces, support local businesses, and engage in civic activities.

This “skin in the game” could foster more civic engagement, better community maintenance, and a renewed sense of ownership over India’s rapidly urbanizing landscape. Cities become communities of stakeholders rather than collections of transient renters.

The Insurance and Risk Mitigation Revolution

Smart contracts could revolutionize property insurance:

Parametric Insurance: Imagine insurance policies embedded directly in tokens. If a building is damaged by a verified natural disaster (confirmed via weather oracles), automatic payouts trigger immediately—no claims process, no paperwork, no waiting months for settlement.

Risk Diversification: Fractional ownership spreads risk across thousands of investors rather than concentrating it in one. If one property faces issues, your portfolio is only minimally affected.

Transparent Claims: All insurance claims and payouts are recorded on-chain, making fraud exponentially harder.

Dynamic Pricing: Insurance premiums could adjust in real-time based on actual building conditions, verified maintenance, and location-specific risk factors.

The Tax Revolution Potential

Here’s a radical thought: Imagine if property taxes were automatically calculated and deducted from rental yields via smart contracts, with receipts recorded on-chain.

No more disputes. No more under-reporting. No more bureaucratic delays. No more corruption at the municipal level.

The government gets guaranteed tax revenue in real-time. Honest taxpayers don’t subsidize tax evaders. Municipal budgets become predictable, enabling better urban planning.

It’s a rare win-win that blockchain uniquely enables, and it could add billions to government coffers while simultaneously reducing compliance costs for property owners.

The Road Ahead: Building the Rails Before the Train Departs

Significant challenges remain before tokenized real estate becomes mainstream. The path is complicated by regulatory uncertainty, the paradox of high asset values clashing with low secondary market liquidity—a direct consequence of the market’s current focus on institutional, buy-and-hold assets rather than high-velocity retail trading—technical fragmentation, and the legal complexity of ensuring an on-chain token is irrefutably linked to its off-chain physical counterpart.

Despite these hurdles, the transformative potential of the underlying technology is undeniable. It represents a fundamental re-architecting of financial infrastructure, moving from siloed, slow, and opaque systems to a more open and efficient model. As one global expert in the space notes, this is a pivotal moment.

“Blockchain is finance’s internet moment. This is the first time we can re-architect how finance is done today at the infrastructure level, and in doing so, create significant business benefits that also benefit end-consumers.”

— Morgan McKenney, CEO of Provenance Blockchain Foundation

“The future is fractional: turning $350 trillion in real-world assets from locked vaults into open markets.”

Tokenization won’t fix broken land laws—but it could leapfrog them. The question isn’t whether India can tokenize real estate. It’s whether we’ll build the rails before the train leaves the station.